Multiples, either from publicly traded comparable companies or transactions, are commonly used in practice to imply values of private companies. But the cannabis industry has several nuances that can limit the use or relevance of traditional earnings multiples in inferring the valuation of other companies.

Use of the market approach (applying multiples to infer a valuation) requires a reasonable data set, both in quantity and quality of comparable companies or transactions. That cannabis companies have a limited history and have been volatile over the last few years are two of the main factors limiting the use and relevance of multiples. The degree of comparability is also a constraint, since jurisdiction, size and stage of development can all have a significant impact on the company’s valuation, not to mention that long-term profitability levels—a main proxy for comparability—are unknown. All’s not lost when it comes to multiples in the cannabis industry.

It’s true that earnings before interest, taxes, depreciation and amortization (EBITDA) multiples are just short of meaningless, since companies are typically pre-profitability. But multiples based on projected revenue or EBITDA, or production capacity can still tell something of a story.

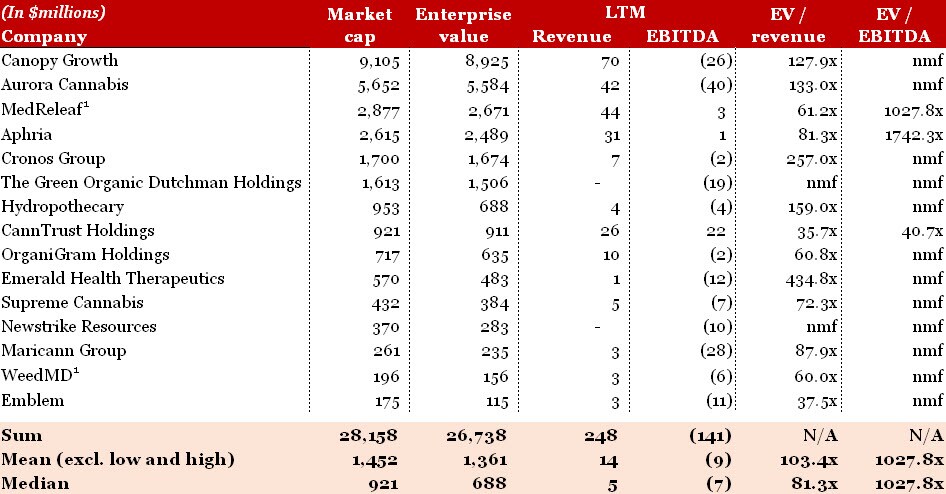

Below is a summary of the market capitalization and implied last 12 months (LTM) revenue and EBITDA multiples of a set of publicly traded cannabis companies, as of June 20, 2018.

Source: Capital IQ, Company Reports, PwC Analysis. Data as at June 20, 2018.

Note 1: Aurora Cannabis entered into an agreement to acquire MedReleaf on May 14, 2018. Hiku Brands entered into an agreement to acquire WeedMD on April 19, 2018. These transactions have yet to close, as at June 20, 2018.

Nmf is not meaningful.

The enterprise value (EV)/LTM revenue multiples traded at an average of 103.4x and a median of 81.3x, as at June 20, 2018. The range of LTM revenue multiples is large, spanning from 35.7x to more than 400x. And size appears to be the primary factor for those companies generating a premium EV/LTM revenue. As can be seen above, EV/LTM EBITDA appears to be not meaningful, due to the state of pre-profitability in the industry prior to legalization. The 15 public companies selected above have made $248 million in revenue and negative $141 million in EBITDA losses over the last 12 months but are collectively worth a total market capitalization of approximately $28 billion.

The sheer size of the multiples and the variability may best be explained by the level of growth that’s anticipated in future cash flows. The current valuations relative to LTM revenues may seem overstated or speculative at first glance. But when potential growth in cash flows is considered resulting from upcoming legalization in Canada and expected legalization in a handful of US states and European countries in the near future, the multiples may start to make more sense.

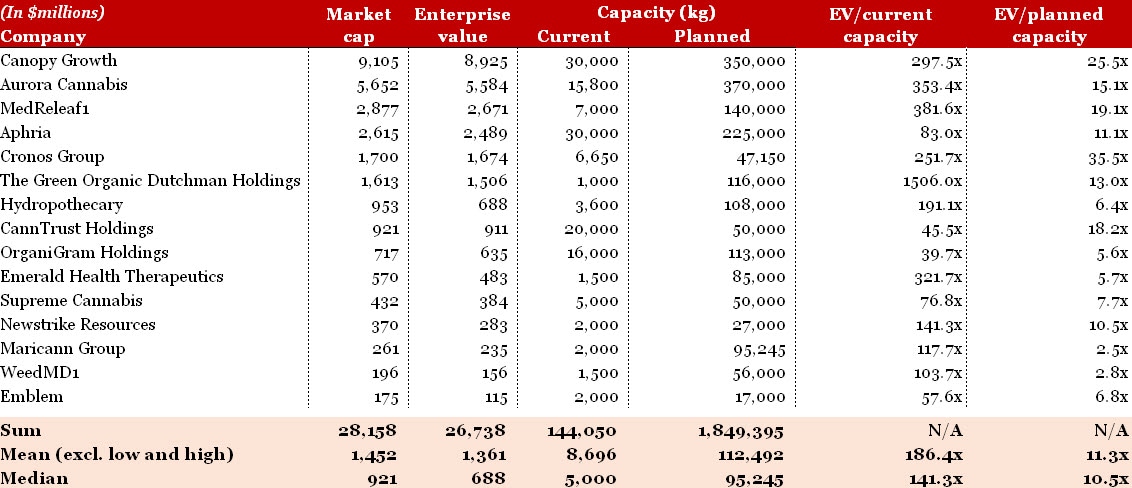

For this reason, cannabis industry–specific multiples focused on production capacity such as EV/current capacity or EV/planned capacity may be more useful for analysis and comparative purposes. To the extent that cash flows are driven or limited by production capacity, the planned production capacity of a company may be more predictive of its near-term profit-generating potential after legalization.

Below is a summary of the implied production capacity multiples of the set of publicly traded cannabis companies, as of June 20, 2018.

Source: Capital IQ, Company Reports, Investor Presentations, PwC Analysis. Data as at June 20, 2018.

Note 1: Aurora Cannabis entered into an agreement to acquire MedReleaf on May 14, 2018. Hiku Brands entered into an agreement to acquire WeedMD on April 19, 2018. These transactions have yet to close, as at June 20, 2018.

The companies above traded at an average EV/current capacity of 186.4x and a median of 141.3x. Although EV/current capacity multiples trade at a wide range of 39.7x to 1,506.0x, the EV/planned capacity multiples are tighter, spanning from 2.5x to 35.5x. The focus of many producers over the last 12 months in Canada has been to scale production capacity in an effort to prepare for the forthcoming legalization of adult-use cannabis. Canopy, Aurora and Aphria are building significant capacity and account for more than half the total planned production capacity above. Companies listed above such as Hydropothecary, Organigram, Emerald and Maricann are close behind and trading at lower EV/planned capacity multiples.

Of note is that the total planned capacity of the 15 public companies selected above is approximately 1.85 million kilograms, and it’s primarily located in Canada. Most industry estimates for the potential long-term domestic demand of cannabis place it at 1 million kilograms (i.e., at maturity). This could imply potential future oversupply of cannabis in the Canadian market. Or it could imply that most management teams are placing a significant bet on potential international export of their products.

Production capacity is critical as these companies look to secure supply agreements with provincial liquor boards. The next critical hurdle will be developing and delivering high-quality, premium products on time and in sufficient quantity to meet supply commitments. Those companies that are successful should be able to create significant revenue and earnings, as well as create substantial value for their shareholders.

With dried flower cannabis and extracts set to become legal later this year and edibles and concentrates expected to be legalized next year, industry consensus is that significant revenue and earnings should start to be generated in 2019.

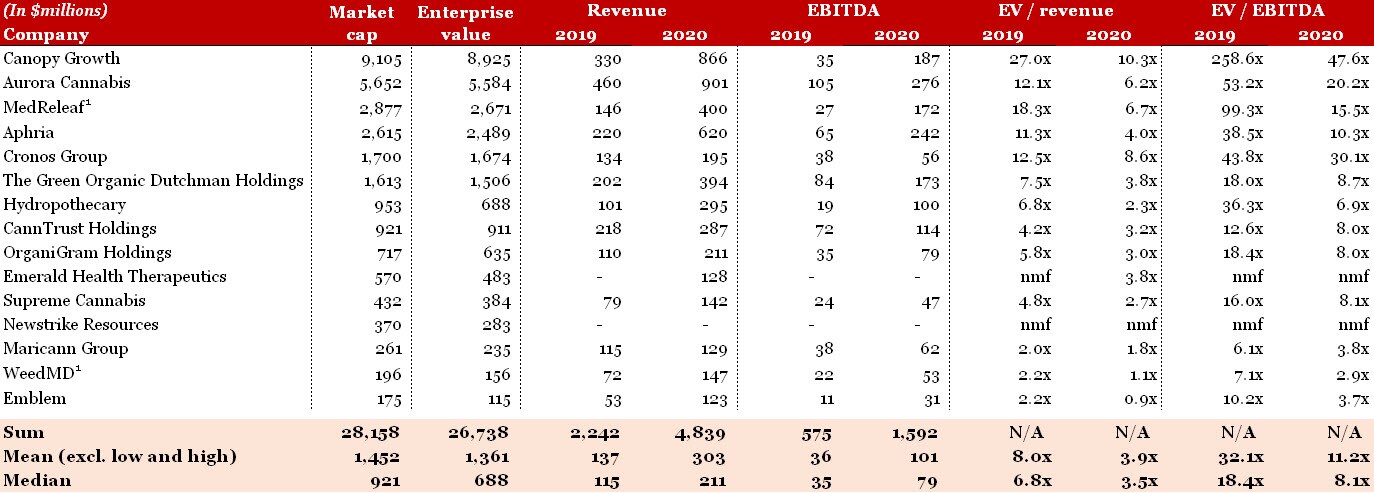

Source: Capital IQ, Company Reports, PwC Analysis. Data as at June 20, 2018.

Note 1: Aurora Cannabis entered into an agreement to acquire MedReleaf on May 14, 2018. Hiku Brands entered into an agreement to acquire WeedMD on April 19, 2018. These transactions have yet to close, as at June 20, 2018.

Nmf is not meaningful.

Looking at the projected revenue and EBITDA estimates above, it becomes increasingly clear that significant international expansion is expected over the next few years. The total revenue estimated to be made in 2020 by only the 15 companies above is approximately $5 billion, which is higher than most estimates of total wholesale revenue for the same period. Cannabis demand in Canada is expected to be approximately 800,000 kilograms in 2020, which could yield total Canadian wholesale revenues of between $3 billion and $4 billion, based on industry estimates1.

The forward EV/revenue and EV/EBITDA multiples for 2019 and 2020 are expected to fall substantially from current levels, as cannabis companies start to create significant revenue and earnings. The average EV/revenue multiple is expected to lower from 103.4x currently to 8.0x in 2019 and 3.9x in 2020, while the average EV/EBITDA multiple is expected to lower from 32.1x in 2019 to 11.2x in 2020. The main question remains whether these companies will be able to achieve these significant revenue and profitability targets. And if not, what will the impact be on their valuations?

The graph below plots the evolution of market capitalization in public cannabis companies that have been trading since early 2015. Notable spikes occurred in December 2015, following the election of a Liberal government promising to legalize cannabis in Canada; December 2016, following American elections where eight states voted to legalize either medical or recreational use; and November 2017, following Constellation Brands’s minority investment in Canopy. While the American elections had a more pronounced impact than their Canadian counterpart, both spikes were followed by a brief drop and then followed by a recovery. Compared to the Canadian and US government decisions, the Constellation event seems to have contributed the biggest increase to market capitalization since 2015.

Source: Capital IQ, PwC Analysis. Data as at June 20, 2018